The function ACF computes an estimate of the autocorrelation function

of a (possibly multivariate) tsibble. Function PACF computes an estimate

of the partial autocorrelation function of a (possibly multivariate) tsibble.

Function CCF computes the cross-correlation or cross-covariance of two columns

from a tsibble.

ACF(

.data,

y,

...,

lag_max = NULL,

type = c("correlation", "covariance", "partial"),

na.action = na.contiguous,

demean = TRUE,

tapered = FALSE

)

PACF(.data, y, ..., lag_max = NULL, na.action = na.contiguous, tapered = FALSE)

CCF(

.data,

y,

x,

...,

lag_max = NULL,

type = c("correlation", "covariance"),

na.action = na.contiguous

)Arguments

- .data

A tsibble

- ...

The column(s) from the tsibble used to compute the ACF, PACF or CCF.

- lag_max

maximum lag at which to calculate the acf. Default is 10*log10(N/m) where N is the number of observations and m the number of series. Will be automatically limited to one less than the number of observations in the series.

- type

character string giving the type of ACF to be computed. Allowed values are

"correlation"(the default),"covariance"or"partial".- na.action

function to be called to handle missing values.

na.passcan be used.- demean

logical. Should the covariances be about the sample means?

- tapered

Produces banded and tapered estimates of the (partial) autocorrelation.

- x, y

a univariate or multivariate (not

ccf) numeric time series object or a numeric vector or matrix, or an"acf"object.

Value

The ACF, PACF and CCF functions return objects

of class "tbl_cf", which is a tsibble containing the correlations computed.

Details

The functions improve the stats::acf(), stats::pacf() and

stats::ccf() functions. The main differences are that ACF does not plot

the exact correlation at lag 0 when type=="correlation" and

the horizontal axes show lags in time units rather than seasonal units.

The resulting tables from these functions can also be plotted using

autoplot() with the methods provided by the ggtime package.

References

Hyndman, R.J. (2015). Discussion of "High-dimensional autocovariance matrices and optimal linear prediction". Electronic Journal of Statistics, 9, 792-796.

McMurry, T. L., & Politis, D. N. (2010). Banded and tapered estimates for autocovariance matrices and the linear process bootstrap. Journal of Time Series Analysis, 31(6), 471-482.

See also

Examples

library(tsibble)

#>

#> Attaching package: ‘tsibble’

#> The following objects are masked from ‘package:base’:

#>

#> intersect, setdiff, union

library(tsibbledata)

library(dplyr)

#>

#> Attaching package: ‘dplyr’

#> The following objects are masked from ‘package:stats’:

#>

#> filter, lag

#> The following objects are masked from ‘package:base’:

#>

#> intersect, setdiff, setequal, union

vic_elec %>% ACF(Temperature)

#> # A tsibble: 47 x 2 [30m]

#> lag acf

#> <cf_lag> <dbl>

#> 1 30m 0.994

#> 2 60m 0.982

#> 3 90m 0.967

#> 4 120m 0.948

#> 5 150m 0.925

#> 6 180m 0.901

#> 7 210m 0.873

#> 8 240m 0.845

#> 9 270m 0.815

#> 10 300m 0.785

#> # ℹ 37 more rows

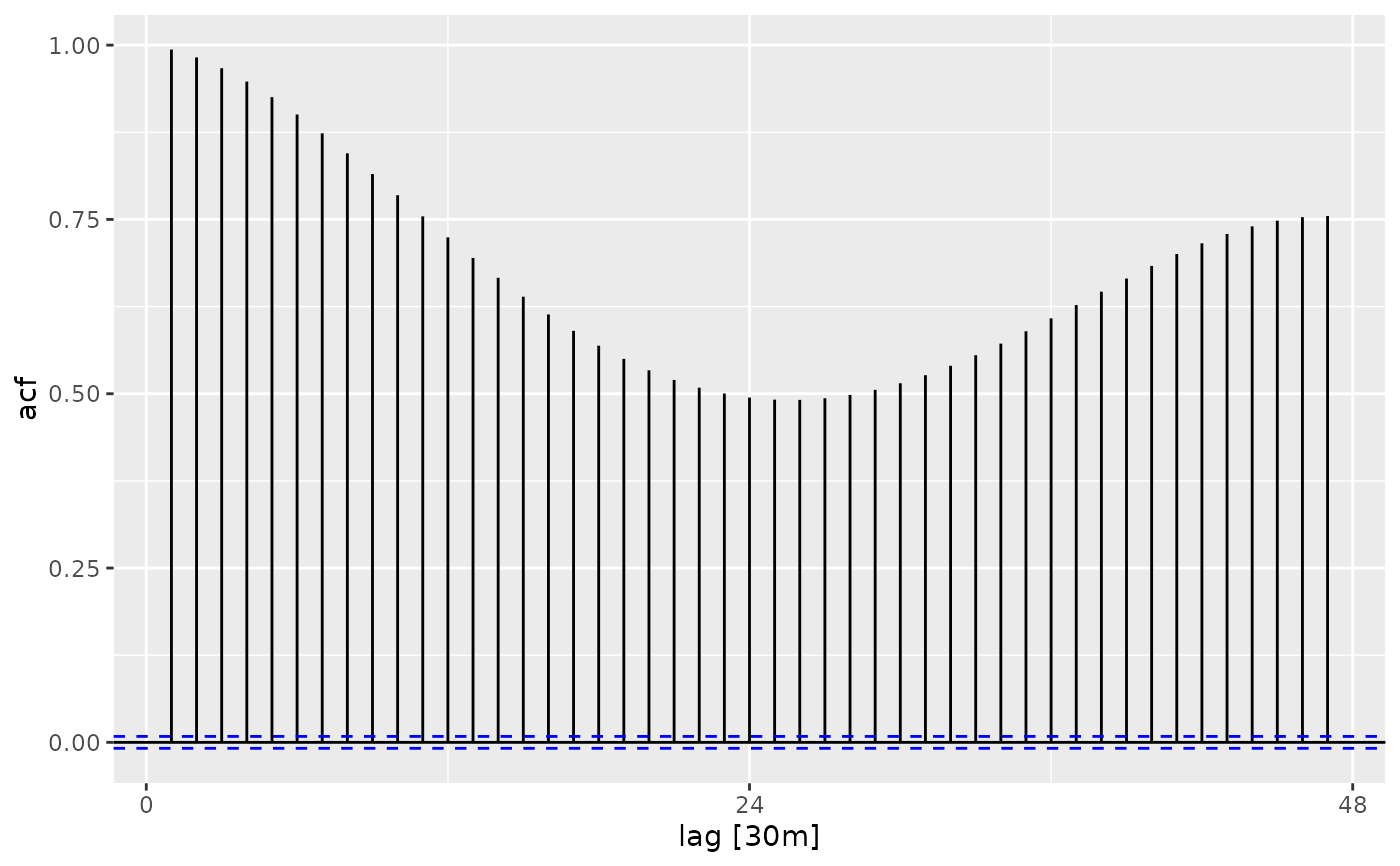

vic_elec %>% ACF(Temperature) %>% autoplot()

#> Plot variable not specified, automatically selected `.vars = acf`

#> Don't know how to automatically pick scale for object of type

#> <cf_lag/vctrs_vctr>. Defaulting to continuous.

vic_elec %>% PACF(Temperature)

#> # A tsibble: 47 x 2 [30m]

#> lag pacf

#> <cf_lag> <dbl>

#> 1 30m 0.994

#> 2 60m -0.395

#> 3 90m -0.220

#> 4 120m -0.141

#> 5 150m -0.0911

#> 6 180m -0.0611

#> 7 210m -0.0252

#> 8 240m -0.0101

#> 9 270m 0.0152

#> 10 300m 0.0169

#> # ℹ 37 more rows

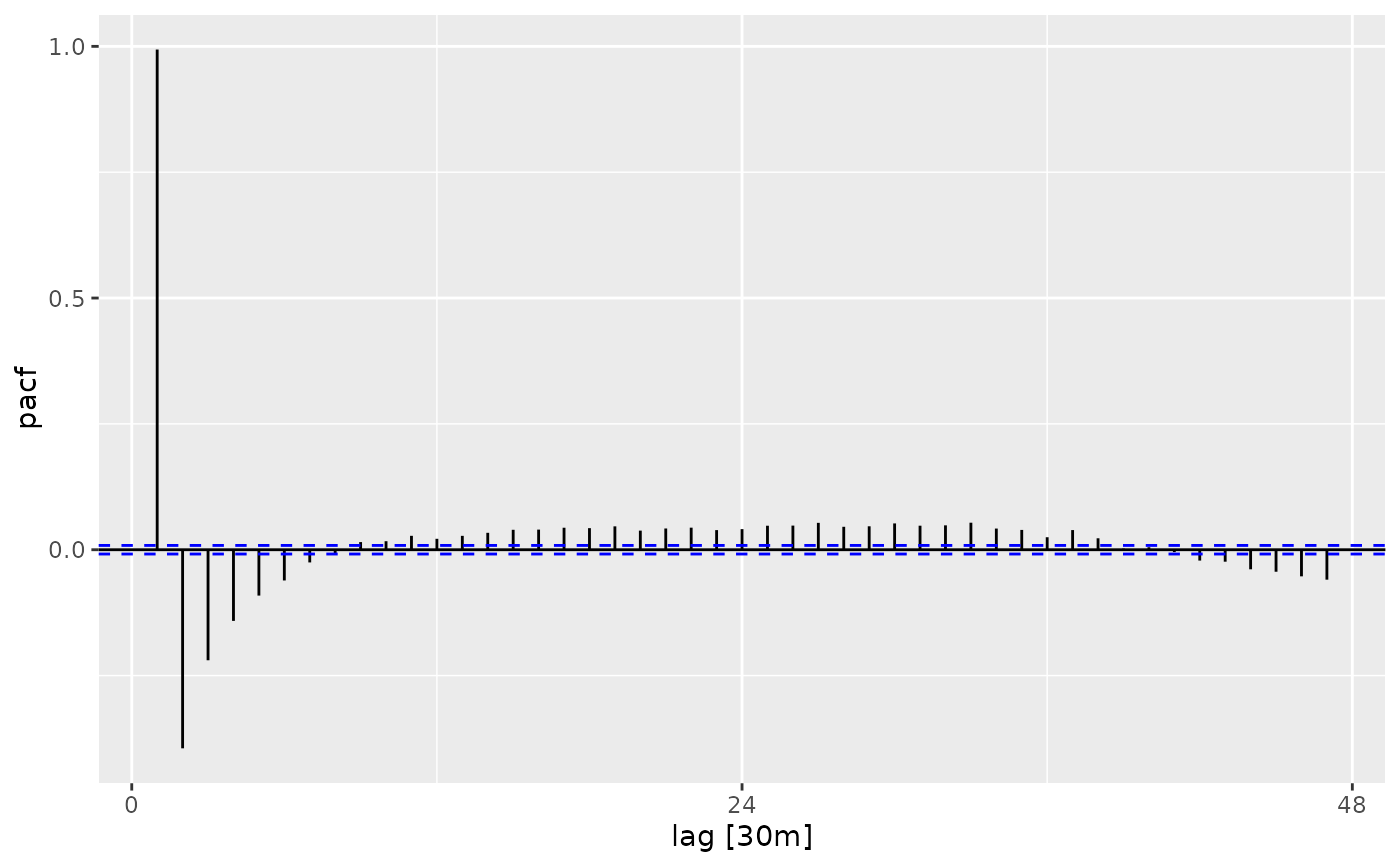

vic_elec %>% PACF(Temperature) %>% autoplot()

#> Plot variable not specified, automatically selected `.vars = pacf`

#> Don't know how to automatically pick scale for object of type

#> <cf_lag/vctrs_vctr>. Defaulting to continuous.

vic_elec %>% PACF(Temperature)

#> # A tsibble: 47 x 2 [30m]

#> lag pacf

#> <cf_lag> <dbl>

#> 1 30m 0.994

#> 2 60m -0.395

#> 3 90m -0.220

#> 4 120m -0.141

#> 5 150m -0.0911

#> 6 180m -0.0611

#> 7 210m -0.0252

#> 8 240m -0.0101

#> 9 270m 0.0152

#> 10 300m 0.0169

#> # ℹ 37 more rows

vic_elec %>% PACF(Temperature) %>% autoplot()

#> Plot variable not specified, automatically selected `.vars = pacf`

#> Don't know how to automatically pick scale for object of type

#> <cf_lag/vctrs_vctr>. Defaulting to continuous.

global_economy %>%

filter(Country == "Australia") %>%

CCF(GDP, Population)

#> # A tsibble: 29 x 3 [1Y]

#> # Key: Country [1]

#> Country lag ccf

#> <fct> <cf_lag> <dbl>

#> 1 Australia -14Y 0.394

#> 2 Australia -13Y 0.427

#> 3 Australia -12Y 0.461

#> 4 Australia -11Y 0.496

#> 5 Australia -10Y 0.530

#> 6 Australia -9Y 0.565

#> 7 Australia -8Y 0.601

#> 8 Australia -7Y 0.637

#> 9 Australia -6Y 0.674

#> 10 Australia -5Y 0.711

#> # ℹ 19 more rows

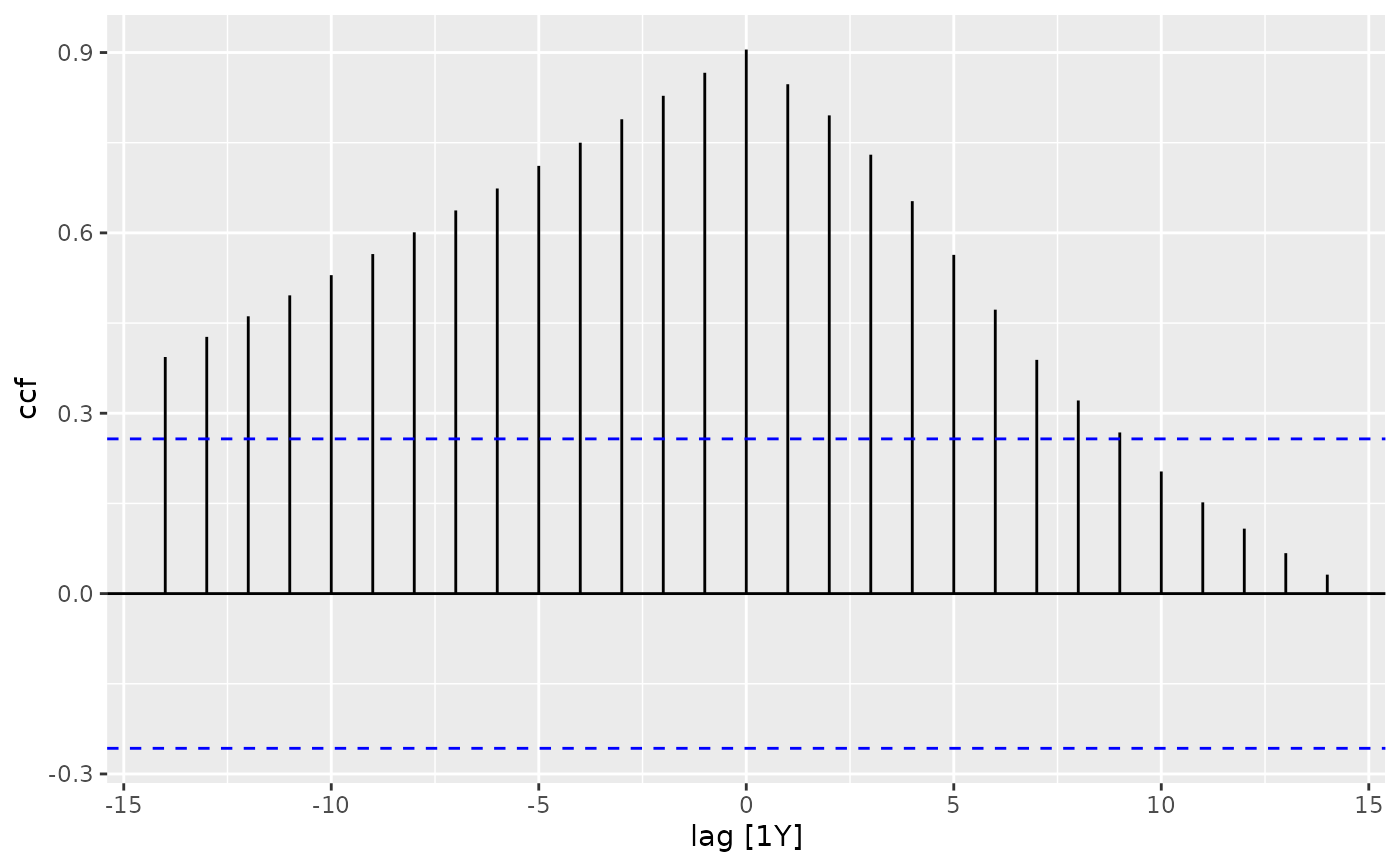

global_economy %>%

filter(Country == "Australia") %>%

CCF(GDP, Population) %>%

autoplot()

#> Plot variable not specified, automatically selected `.vars = ccf`

#> Don't know how to automatically pick scale for object of type

#> <cf_lag/vctrs_vctr>. Defaulting to continuous.

global_economy %>%

filter(Country == "Australia") %>%

CCF(GDP, Population)

#> # A tsibble: 29 x 3 [1Y]

#> # Key: Country [1]

#> Country lag ccf

#> <fct> <cf_lag> <dbl>

#> 1 Australia -14Y 0.394

#> 2 Australia -13Y 0.427

#> 3 Australia -12Y 0.461

#> 4 Australia -11Y 0.496

#> 5 Australia -10Y 0.530

#> 6 Australia -9Y 0.565

#> 7 Australia -8Y 0.601

#> 8 Australia -7Y 0.637

#> 9 Australia -6Y 0.674

#> 10 Australia -5Y 0.711

#> # ℹ 19 more rows

global_economy %>%

filter(Country == "Australia") %>%

CCF(GDP, Population) %>%

autoplot()

#> Plot variable not specified, automatically selected `.vars = ccf`

#> Don't know how to automatically pick scale for object of type

#> <cf_lag/vctrs_vctr>. Defaulting to continuous.